Issued a 250 Credit Memorandum to Art Co For an Allowance on Goods Sold on July 18

Merchandising Transactions

33 Analyze and Record Transactions for the Sale of Merchandise Using the Perpetual Inventory Organisation

The following example transactions and subsequent journal entries for merchandise sales are recognized using a perpetual inventory system. The periodic inventory organization recognition of these instance transactions and corresponding periodical entries are shown in Appendix: Clarify and Record Transactions for Trade Purchases and Sales Using the Periodic Inventory Organization.

Basic Analysis of Sales Transaction Journal Entries

Permit's continue to follow California Business organisation Solutions (CBS) and their sales of electronic hardware packages to business customers. As previously stated, each package contains a desktop figurer, tablet computer, landline telephone, and a 4-in-i printer. CBS sells each hardware package for $1,200. They offer their customers the selection of purchasing extra private hardware items for every electronic hardware package purchase. (Figure) lists the products CBS sells to customers; the prices are per-bundle, and per unit.

CBS's Product Line. (attribution: Copyright Rice University, OpenStax, nether CC BY-NC-SA 4.0 license)

Cash and Credit Sales Transaction Periodical Entries

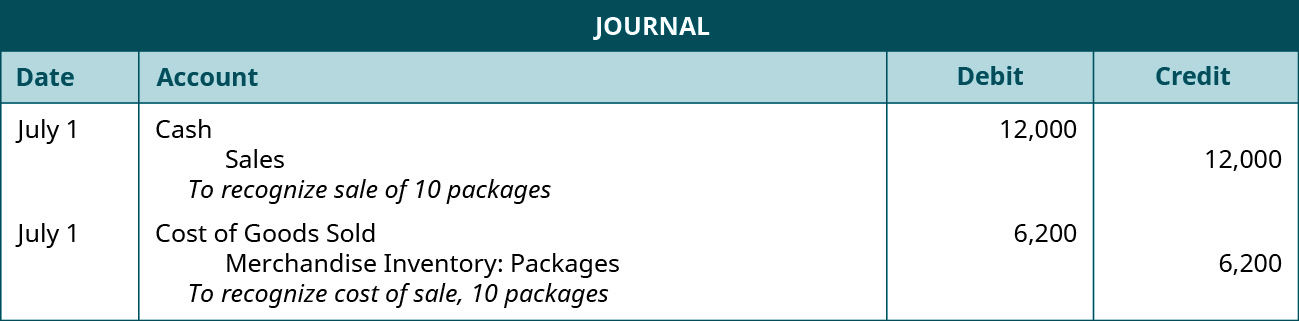

On July 1, CBS sells 10 electronic hardware packages to a customer at a sales toll of $1,200 each. The customer pays immediately with cash. The following entries occur.

In the starting time entry, Cash increases (debit) and Sales increases (credit) for the selling toll of the packages, $12,000 ($1,200 × ten). In the second entry, the cost of the sale is recognized. COGS increases (debit) and Merchandise Inventory-Packages decreases (credit) for the cost of the packages, $6,200 ($620 × 10).

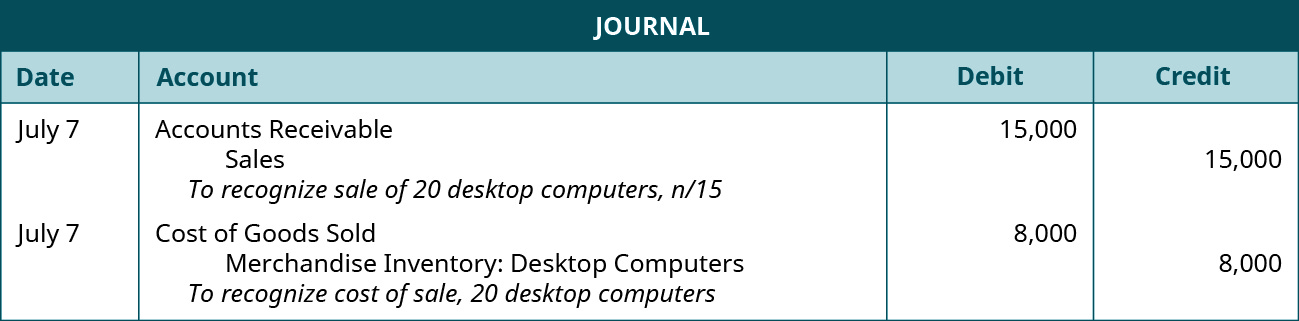

On July 7, CBS sells twenty desktop computers to a customer on credit. The credit terms are north/xv with an invoice date of July seven. The following entries occur.

Since the computers were purchased on credit by the customer, Accounts Receivable increases (debit) and Sales increases (credit) for the selling price of the computers, $15,000 ($750 × 20). In the second entry, Merchandise Inventory-Desktop Computers decreases (credit), and COGS increases (debit) for the toll of the computers, $8,000 ($400 × 20).

On July 17, the customer makes total payment on the corporeality due from the July vii sale. The following entry occurs.

Accounts Receivable decreases (credit) and Cash increases (debit) for the full amount owed. The credit terms were n/15, which is internet due in 15 days. No disbelieve was offered with this transaction; thus the full payment of $xv,000 occurs.

Sales Discount Transaction Journal Entries

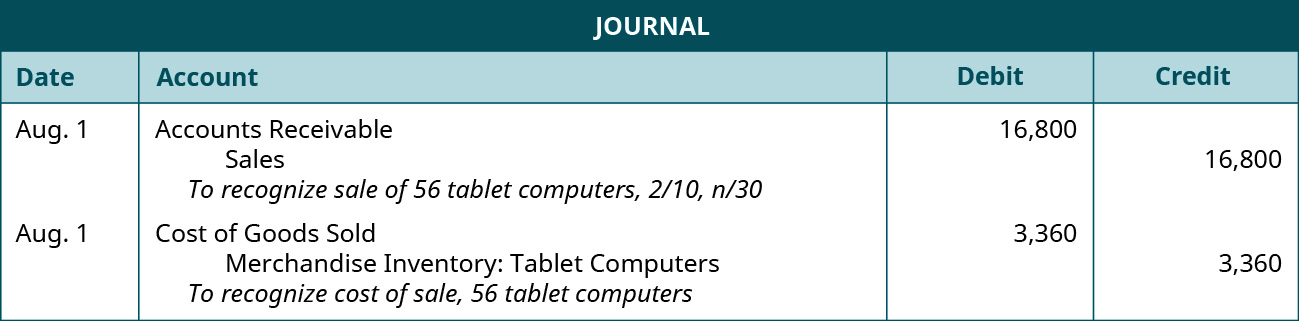

On Baronial 1, a client purchases 56 tablet computers on credit. The payment terms are 2/10, northward/thirty, and the invoice is dated Baronial one. The post-obit entries occur.

In the first entry, both Accounts Receivable (debit) and Sales (credit) increase by $16,800 ($300 × 56). These credit terms are a little different than the earlier case. These credit terms include a discount opportunity (2/10), meaning the client has 10 days from the invoice date to pay on their account to receive a 2% discount on their purchase. In the 2d entry, COGS increases (debit) and Merchandise Inventory–Tablet Computers decreases (credit) in the amount of $3,360 (56 × $60).

On Baronial 10, the customer pays their account in total. The following entry occurs.

Since the customer paid on Baronial 10, they made the 10-solar day window and received a discount of ii%. Cash increases (debit) for the amount paid to CBS, less the disbelieve. Sales Discounts increases (debit) for the amount of the discount ($xvi,800 × 2%), and Accounts Receivable decreases (credit) for the original amount owed, earlier discount. Sales Discounts volition reduce Sales at the cease of the period to produce net sales.

Let'south accept the same example sale with the same credit terms, simply now assume the customer paid their business relationship on Baronial 25. The post-obit entry occurs.

Cash increases (debit) and Accounts Receivable decreases (credit) by $16,800. The customer paid on their account outside of the disbelieve window only within the total allotted timeframe for payment. The customer does not receive a discount in this instance but does pay in full and on time.

Recording a Retailer's Sales Transactions

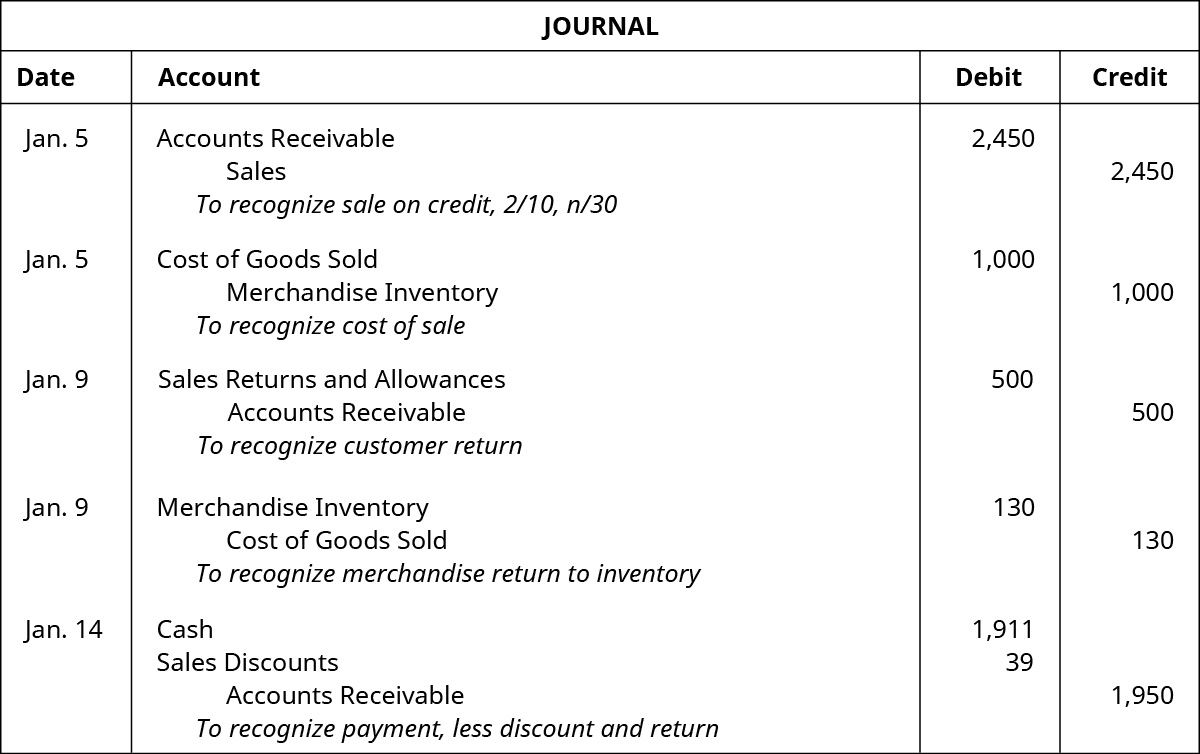

Record the journal entries for the following sales transactions by a retailer.

| Jan. 5 | Sold $2,450 of trade on credit (cost of $i,000), with terms two/10, n/30, and invoice dated January five. |

| Jan. 9 | The client returned $500 worth of slightly damaged trade to the retailer and received a full refund. The retailer returned the merchandise to its inventory at a price of $130. |

| January. fourteen | Business relationship paid in full. |

Solution

Sales Returns and Allowances Transaction Journal Entries

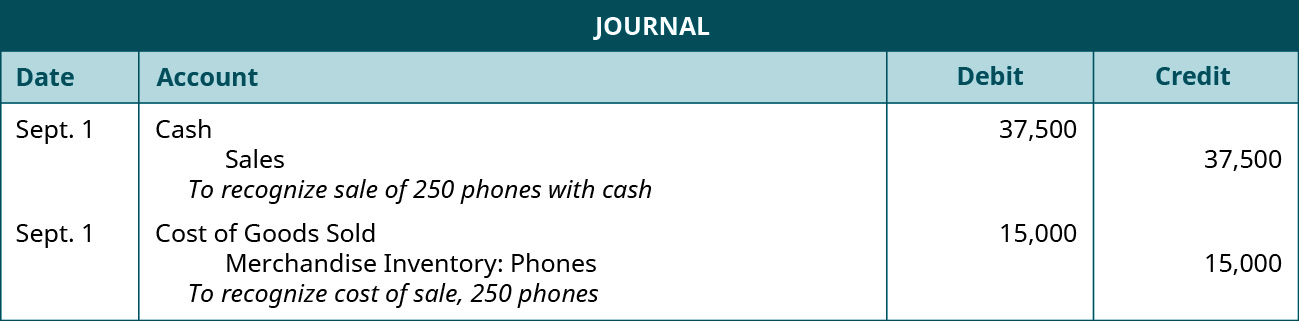

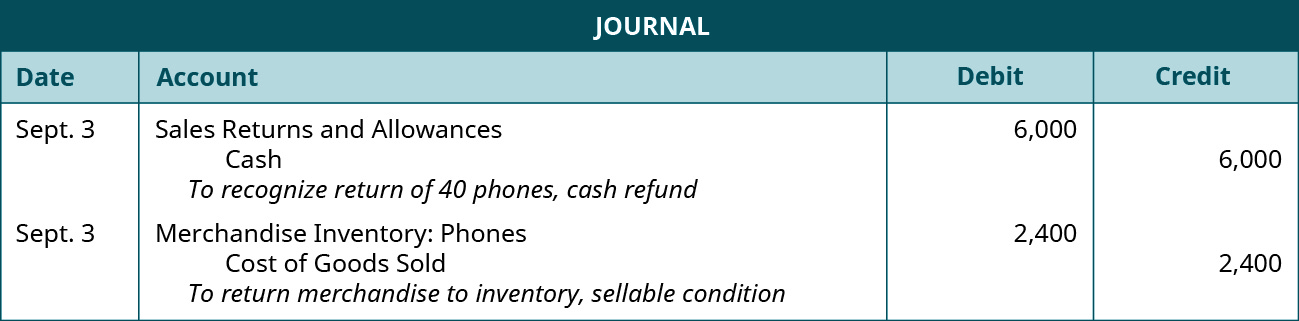

On September i, CBS sold 250 landline telephones to a customer who paid with cash. On September 3, the customer discovers that xl of the phones are the wrong color and returns the phones to CBS in exchange for a full refund. CBS determines that the returned merchandise can exist resold and returns the merchandise to inventory at its original cost. The post-obit entries occur for the sale and subsequent return.

In the commencement entry on September 1, Cash increases (debit) and Sales increases (credit) by $37,500 (250 × $150), the sales price of the phones. In the second entry, COGS increases (debit), and Merchandise Inventory-Phones decreases (credit) by $fifteen,000 (250 × $60), the cost of the sale.

Since the customer already paid in full for their purchase, a full cash refund is issued on September 3. This increases Sales Returns and Allowances (debit) and decreases Cash (credit) by $six,000 (xl × $150). The 2d entry on September 3 returns the phones back to inventory for CBS because they have determined the merchandise is in sellable condition at its original price. Merchandise Inventory–Phones increases (debit) and COGS decreases (credit) past $2,400 (forty × $threescore).

On September 8, the customer discovers that 20 more phones from the September i purchase are slightly damaged. The customer decides to continue the phones but receives a sales allowance from CBS of $10 per phone. The post-obit entry occurs for the assart.

Since the customer already paid in full for their purchase, a cash refund of the allowance is issued in the amount of $200 (twenty × $10). This increases (debit) Sales Returns and Allowances and decreases (credit) Greenbacks. CBS does not have to consider the condition of the merchandise or return it to their inventory because the customer keeps the merchandise.

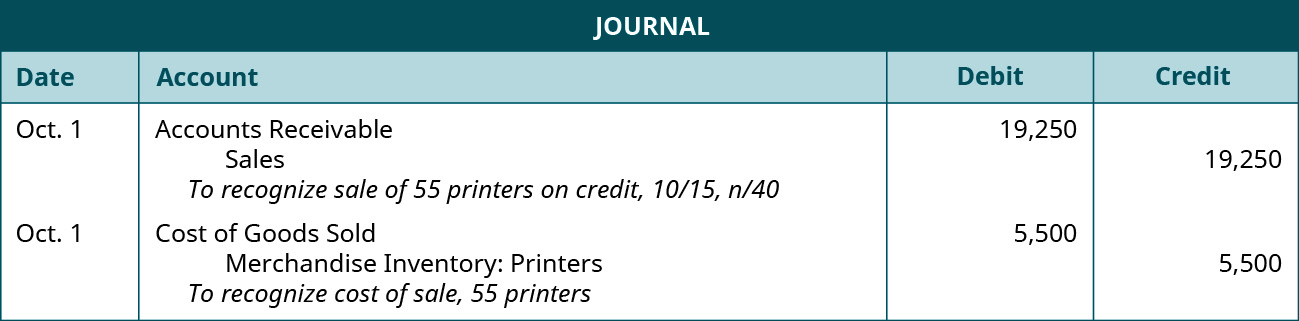

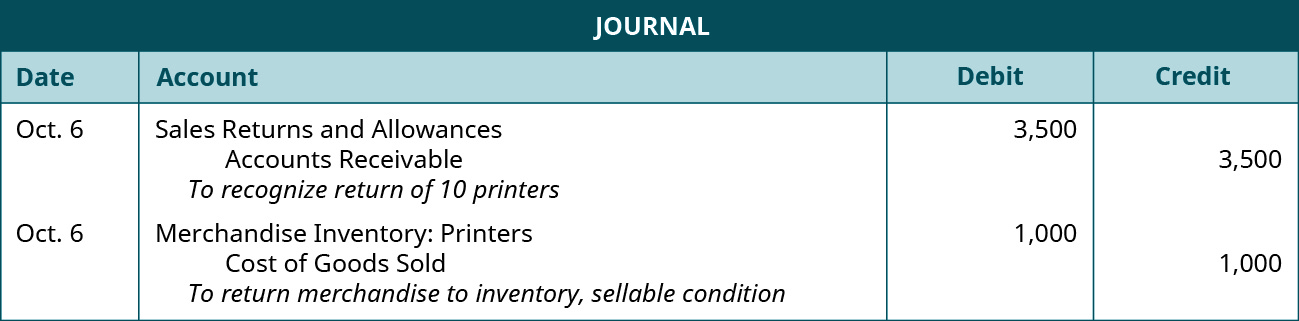

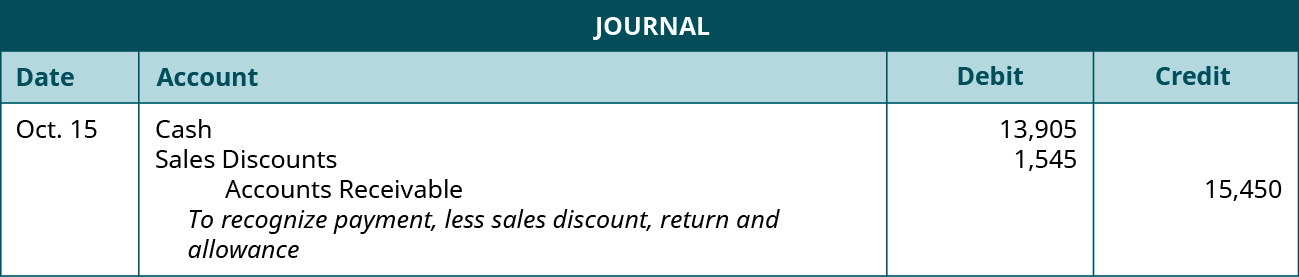

A customer purchases 55 units of the 4-in-1 desktop printers on October one on credit. Terms of the sale are ten/15, due north/40, with an invoice date of Oct 1. On Oct 6, the customer returned 10 of the printers to CBS for a full refund. CBS returns the printers to their inventory at the original cost. The following entries show the sale and subsequent return.

In the start entry on October ane, Accounts Receivable increases (debit) and Sales increases (credit) by $19,250 (55 × $350), the sales price of the printers. Accounts Receivable is used instead of Greenbacks because the customer purchased on credit. In the second entry, COGS increases (debit) and Merchandise Inventory–Printers decreases (credit) by $v,500 (55 × $100), the cost of the sale.

The client has not yet paid for their buy as of October six. Therefore, the return increases Sales Returns and Allowances (debit) and decreases Accounts Receivable (credit) by $iii,500 (ten × $350). The second entry on Oct 6 returns the printers back to inventory for CBS because they take determined the merchandise is in sellable condition at its original cost. Trade Inventory–Printers increases (debit) and COGS decreases (credit) by $1,000 (10 × $100).

On Oct 10, the customer discovers that 5 printers from the October i purchase are slightly damaged, but decides to go on them, and CBS problems an assart of $sixty per printer. The following entry recognizes the allowance.

Sales Returns and Allowances increases (debit) and Accounts Receivable decreases (credit) by $300 (v × $60). A reduction to Accounts Receivable occurs considering the client has yet to pay their account on Oct 10. CBS does not accept to consider the condition of the merchandise or return it to their inventory because the customer keeps the merchandise.

On October 15, the customer pays their account in full, less sales returns and allowances. The following payment entry occurs.

Accounts Receivable decreases (credit) for the original amount owed, less the render of $3,500 and the allowance of $300 ($19,250 – $3,500 – $300). Since the customer paid on Oct 15, they made the xv-day window, thus receiving a disbelieve of 10%. Sales Discounts increases (debit) for the discount corporeality ($fifteen,450 × 10%). Cash increases (debit) for the amount owed to CBS, less the discount.

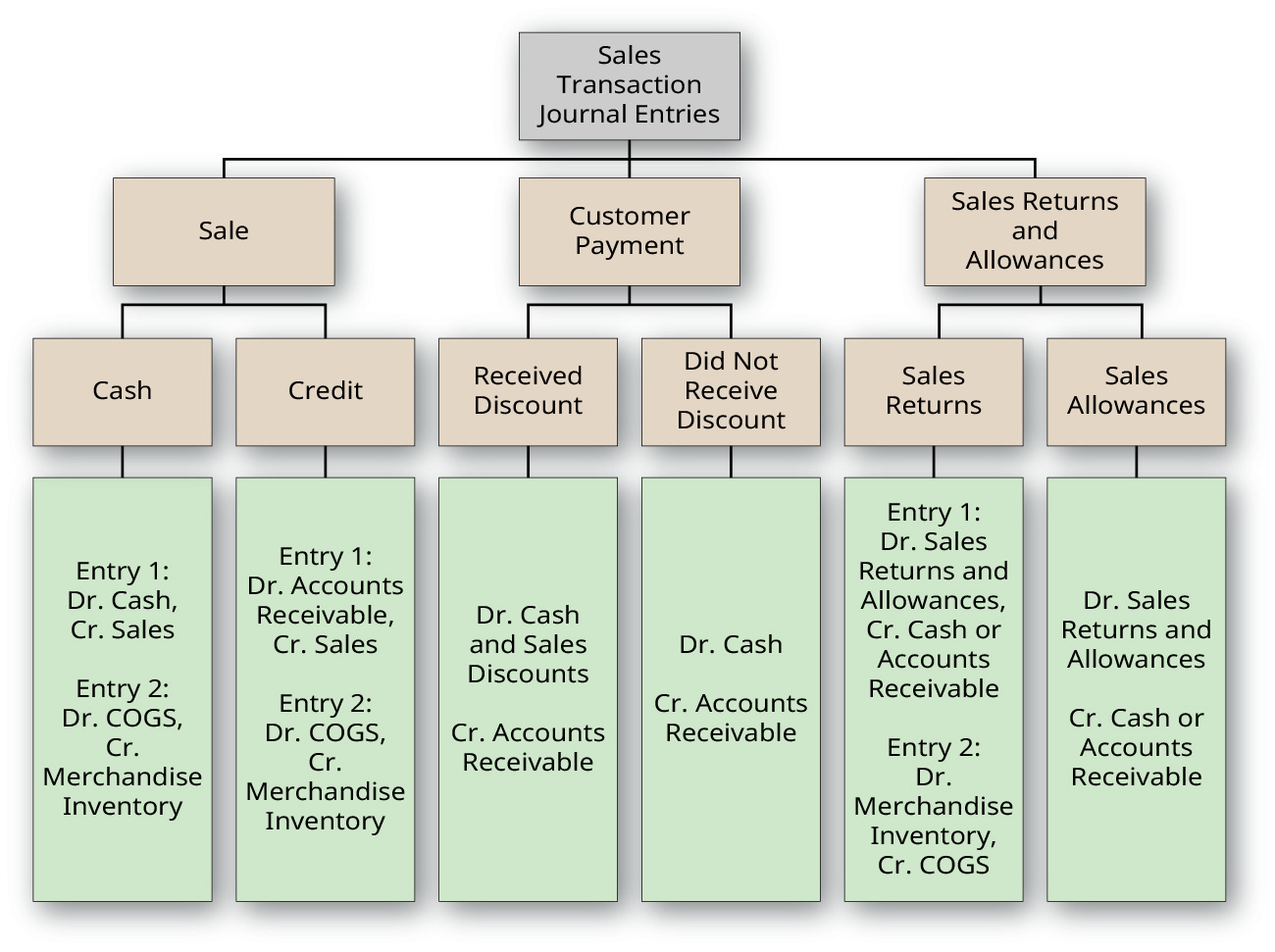

Summary of Sales Transaction Periodical Entries

The chart in (Figure) represents the journal entry requirements based on diverse merchandising sales transactions.

Journal Entry Requirements for Merchandise Sales Transaction. (attribution: Copyright Rice Academy, OpenStax, nether CC BY-NC-SA 4.0 license)

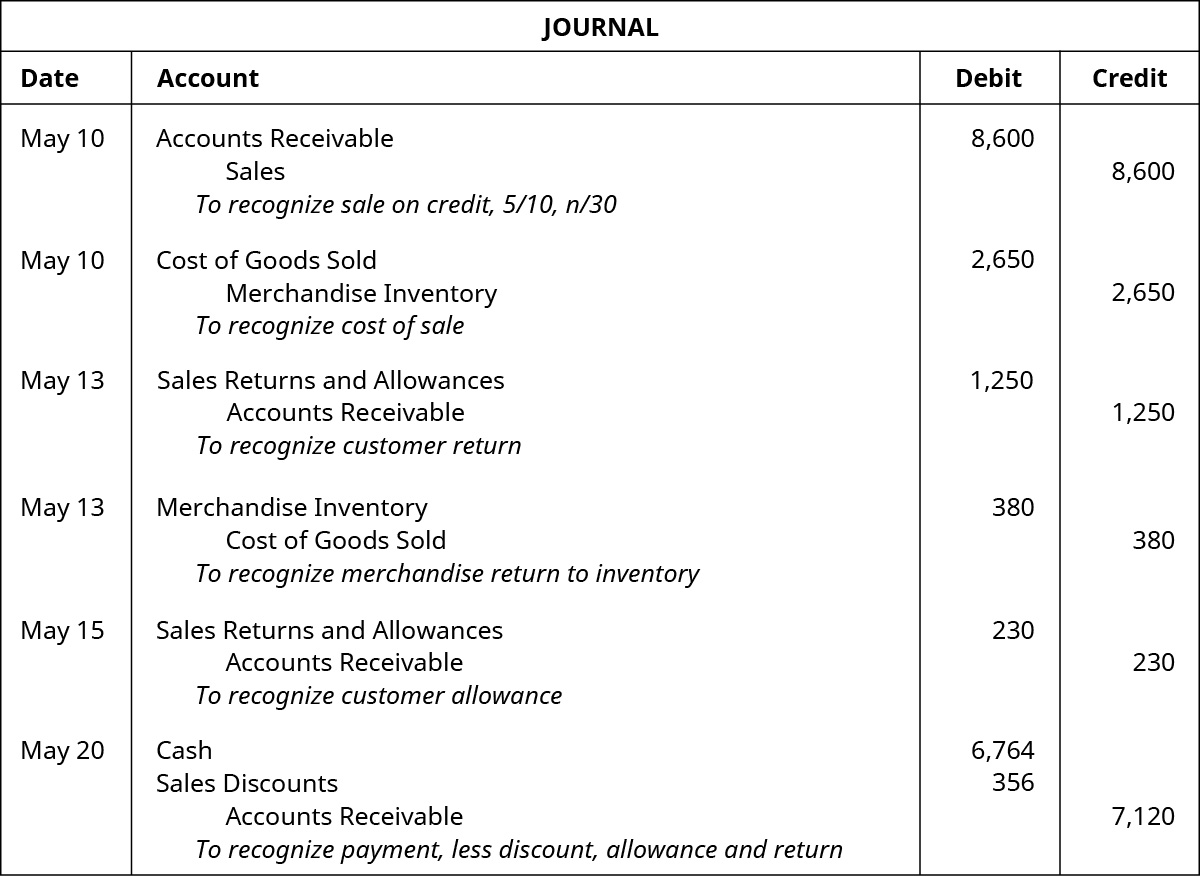

Recording a Retailer's Sales Transactions

Record the journal entries for the following sales transactions of a retailer.

| May 10 | Sold $8,600 of merchandise on credit (price of $2,650), with terms 5/10, n/30, and invoice dated May ten. |

| May 13 | The customer returned $1,250 worth of slightly damaged trade to the retailer and received a total refund. The retailer returned the merchandise to its inventory at a price of $380. |

| May 15 | The client discovered some trade were the wrong color and received an assart from the retailer of $230. |

| May xx | The customer paid the account in total, less the return and allowance. |

Solution

Key Concepts and Summary

- A customer can pay with cash or on credit. If paying on credit instead of greenbacks, Accounts Receivable increases rather than Cash; Sales increases in both instances. A visitor must also record the cost of sale entry, where Merchandise Inventory decreases and COGS increases.

- If a client pays for merchandise within the disbelieve window, the visitor would debit Cash and Sales Discounts while crediting Accounts Receivable. If the customer pays outside the disbelieve window, the company debits Cash and credits Accounts Receivable only.

- If a customer returns merchandise before remitting payment, the company would debit Sales Returns and Allowances and credit Accounts Receivable or Cash. The company may render the merchandise to their inventory by debiting Merchandise Inventory and crediting COGS.

- If a client obtains an assart for damaged merchandise before remitting payment, the company would debit Sales Returns and Allowances and credit Accounts Receivable or Cash. The company does not have to consider the merchandise condition because the customer keeps the merchandise in this instance.

Multiple Selection

(Effigy)Which of the following accounts are used when recording the sales entry of a sale on credit?

- trade inventory, cash

- accounts receivable, merchandise inventory

- accounts receivable, sales

- sales, cost of appurtenances sold

(Effigy)A client pays on credit for $1,250 worth of merchandise, terms iv/15, n/30. If the client pays within the disbelieve window, how much volition they remit in greenbacks to the retailer?

- $1,250

- $1,200

- $l

- $500

(Figure)A customer returns $870 worth of merchandise and receives a full refund. What accounts recognize this sales return (disregarding the merchandise status entry) if the return occurs before the customer remits payment to the retailer?

- accounts receivable, sales returns and allowances

- accounts receivable, cash

- sales returns and allowances, trade inventory

- accounts receivable, price of appurtenances sold

Questions

(Figure)Name two situations where cash would exist remitted to a customer from a retailer later on purchase.

(Figure)If a customer purchased merchandise in the amount of $340, terms 3/10, n/30, returned $70 of the inventory for a total refund, and received an allowance for $65, how much discount would be applied if the customer remitted payment inside the discount window?

(Figure)A customer discovers 60% of the total merchandise delivered from a retailer is damaged. The original buy for all trade was $3,600. The client decides to return 35% of the damaged trade for a total refund and keep the remaining 65%. What is the value of the merchandise returned?

Do Set up A

(Figure)Tape journal entries for the following sales transactions of Flower Visitor.

| October. 12 | Sold 25 bushels of flowers to a client for $ane,000 cash; cost of auction $700. |

| Oct. 21 | Sold 40 bushels of flowers for $30 per bushel on credit. Terms of the sale are 4/x, n/30, invoice dated October 21. Toll per bushel is $xx to Flower Company. |

| Oct. 31 | Received payment in full from the October 21 sale. |

(Figure)Record the journal entries for the following sales transactions of Apache Industries.

| Nov. 7 | Sold 10 computers on credit for $870 per calculator. Terms of the sale are 5/x, due north/threescore, invoice dated Nov vii. The cost per estimator to Apache is $560. |

| Nov. xiv | The client returned 2 computers for a full refund from Apache. Apache returns the computers to their inventory at full toll of $560 per computer. |

| Nov. 21 | The customer paid their account in total from the Nov 7 sale. |

(Effigy)Record the journal entry or entries for each of the following sales transactions. Glow Industries sells 240 strobe lights at $40 per light to a customer on May 9. The cost to Glow is $23 per light. The terms of the sale are five/xv, north/40, invoice dated May ix. On May 13, the customer discovers fifty of the lights are the wrong color and are granted an allowance of $10 per lite for the error. On May 21, the customer pays for the lights, less the assart.

Exercise Set B

(Effigy)Blue Barns sold 136 gallons of paint at $31 per gallon on July 6 to a customer with a toll of $nineteen per gallon to Blue Barns. Terms of the auction are 2/fifteen, due north/45, invoice dated July 6. The customer pays their account in full on July 24. On July 28, the customer discovers 17 gallons are the wrong colour and returns the paint for a total cash refund. Blue Barns returns the gallons to their inventory at the original cost per gallon. Tape the journal entries to recognize these transactions for Blue Barns.

(Effigy)Canary Lawnmowers sold 70 lawnmower parts at $v.00 per part to a customer on December four with a cost to Canary of $three.00 per part. Terms of the sale are 5/10, n/25, invoice dated December 4. The customer pays their account in full on December 16. On December 21, the client discovers 22 of the parts are the wrong size but decides to keep them after Canary gives them an allowance of $one.00 per part. Record the journal entries to recognize these transactions for Canary Lawnmowers.

(Figure)Tape journal entries for the following sales transactions of Balloon Depot.

| Mar. eight | Sold 570 balloon bundles to a client on credit for $38 per package. The cost to Airship Depot was $25 per parcel. Terms of the auction are 3/10, n/xxx, invoice dated March 8. |

| Mar. xi | The customer returned 70 bundles for a total refund from Airship Depot. Balloon Depot returns the balloons to their inventory at the original cost of $25 per bundle. |

| Mar. 18 | The customer paid their account in full from the March 8 buy. |

Problem Set A

(Effigy)Review the following sales transactions for Birdy Birdhouses and tape whatsoever required periodical entries.

| Aug. 10 | Birdy Birdhouses sells 20 birdhouses to client Julia Brand at a cost of $70 each in exchange for cash. The toll to Birdy is $46 per birdhouse. |

| Aug. 12 | Birdy Birdhouses sells thirty birdhouses to customer Julia Make at a price of $68 each on credit. The cost of auction for Birdy is $44 per birdhouse. Terms of the sale are 2/10, n/30, invoice date August 12. |

| Aug. 14 | Julia discovers 6 of the birdhouses are slightly damaged from the August 10 purchase and returns them to Birdy for a total refund. Julia likewise discovers that x of the birdhouses from the Baronial 12 buy are painted the wrong color simply keeps them since Birdy granted an allowance of $24 per birdhouse. |

| Aug. 20 | Julia pays her account in full from the August 12 purchase, less whatsoever returns, allowances, and/or discounts. |

(Figure)Review the post-obit sales transactions for Dish Mart and tape any required journal entries. Notation that all sales transactions are with the aforementioned customer, Emma Purcell.

| Mar. 5 | Dish Mart fabricated a cash sale of 13 sets of dishes at a price of $700 per set to client Emma Purcell. The cost per set is $460 to Dish Mart. |

| Mar. 9 | Dish Mart sold 23 sets of dishes to Emma for $650 per fix on credit, at a price to Dish Mart of $435 per fix. Terms of the sale are five/15, n/60, invoice engagement March 9. |

| Mar. 13 | Emma returns 8 of the dish sets from the March 9 sale to Dish Mart for a full refund. Dish Mart returns the dish sets to inventory at their original cost of $435 per set. |

| Mar. 14 | Dish Mart sells vi sets of dishes to Emma for $670 per assault credit, at a cost to Dish Mart of $450 per set. Terms of the auction are 5/10, northward/60, invoice date March 14. |

| Mar. 15 | Emma discovers that iii of the dish sets from the March 14 purchase, and 7 of the dish sets from the March five sale are missing a few dishes, but keeps them since Dish Mart granted an allowance of $2,670 for all ten dish sets. Dish Mart and Emma have agreed to reduce the corporeality Dish Mart has outstanding instead of sending a carve up cheque for the March 5 allowance in cash. |

| Mar. 24 | Emma Purcell pays her account in full for all outstanding purchases, less whatsoever returns, allowances, and/or discounts. |

Problem Set B

(Figure)Review the following sales transactions for April Anglers and tape any required journal entries.

| Oct. 4 | April Anglers made a greenbacks sale of 40 fishing poles to customer Billie Dyer at a toll of $55 per pole. The cost to April is $33 per pole. |

| Oct. five | April Anglers sells 24 angling poles to customer Billie Dyer at a cost of $52 per pole on credit. The cost to April is $30 per pole. Terms of the sale are ii/x, n/30, invoice date October 5. |

| Oct. 12 | Billie returns seven of the fishing poles from the Oct 4 purchase to April Anglers for a full refund. April returns these poles to their inventory at the original cost per pole. Billie also discovers that 6 of the fishing poles from the Oct 5 buy are the wrong colour but keeps them since Apr granted an assart of $18 per line-fishing pole. |

| Oct. 24 | Apr pays their account in full from the October 5 purchase, less any returns, allowances, and/or discounts. |

(Effigy)Review the post-obit sales transactions for Dish Mart and record any required periodical entries. Note that all sales transactions are with the same customer, Bella Davies.

| Apr. 5 | Dish Mart made a greenbacks sale of 22 sets of cutlery to Bella Davies for $330 per fix. The cost per set to Dish Mart is $125 per set. |

| Apr. 9 | Dish Mart sells 14 sets of cutlery to Bella Davies on credit for $345 per set. The toll per prepare to Dish Mart is $120 per prepare. Terms of the auction are 2/15, n/lx, invoice date April ix. |

| Apr. xiii | Bella returns 9 of the cutlery sets from the Apr 9 auction to Dish Mart for a total refund. Dish Mart restores the cutlery to its inventory at the original cost of $120 per set. |

| Apr. 14 | Bella purchases 18 sets of cutlery for $275 per set on credit, at a cost to Dish Mart of $124 per set. Terms of the sale are 2/x, n/60, invoice date April 14. |

| Apr. fifteen | Bella discovers that 5 of the cutlery sets from the Apr 14 purchase and 10 of the cutlery sets from the April 5 purchase are missing a few spoons merely keeps them since Dish Mart granted an allowance of $175 per set for all dish sets. Dish Mart and Bella have agreed to reduce the amount Bella has outstanding instead of sending a separate bank check for the April 5 allowance in cash. |

| Apr. 28 | Bella Davies pays her account in full for all outstanding purchases, less any returns, allowances, and/or discounts. |

Source: https://opentextbc.ca/principlesofaccountingv1openstax/chapter/analyze-and-record-transactions-for-the-sale-of-merchandise-using-the-perpetual-inventory-system/

0 Response to "Issued a 250 Credit Memorandum to Art Co For an Allowance on Goods Sold on July 18"

Post a Comment